Autor

Jonathan Hobbs, CFA

Fecha

29 May 2026

Categoría

Investor update

How Options Income ETPs Fit into Model Portfolios

Su capital está en riesgo si invierte. Podría perder toda su inversión. Por favor, consulte la advertencia de riesgos completa aquí.

Many wealth managers and advisers use model portfolios to invest for their clients. These combine stocks, bonds, and sometimes alternative assets into pre-built mixes, which they apply across multiple client accounts. Some model portfolios aim to deliver income – but that income is getting harder to find.

This article explains how options income exchange-traded products (ETPs) could help generate more income – and where they may fit into model portfolios.

Why model portfolios may need new income sources

Some model portfolios aim to pay investors a target income. Traditionally, that income comes from stock dividends, bond coupons, and property exposure. But each income source has its limits today.

Dividends have fallen over time. The S&P 500's dividend yield is now just over 1% – below its dot-com low. European stocks pay higher dividends, but not by much. The STOXX Europe 600 and the FTSE 100 both have dividend yields of around 3%.

Bond coupons are currently higher, but they can swing with interest rate cycles. According to Nareit, REITs currently yield around 3.7%. But rising interest rates have generally raised borrowing costs and weighed on valuations.

Income models already spread income across several sources. Options income could be another – and that's where these funds might come in.

Options income strategies can earn cash by selling options on an asset. The seller collects a premium upfront – much like an insurer collects a premium for taking on risk. Covered calls hold the asset and sell call options on it. Cash-secured puts hold cash and sell put options. Either way, the premium is the source of income.

Where options income ETPs might work in a model portfolio

Options strategies can produce income from almost any asset with a liquid options market. So a manager could decide how much to allocate to options income, then fund it by trimming the exposures it most resembles.

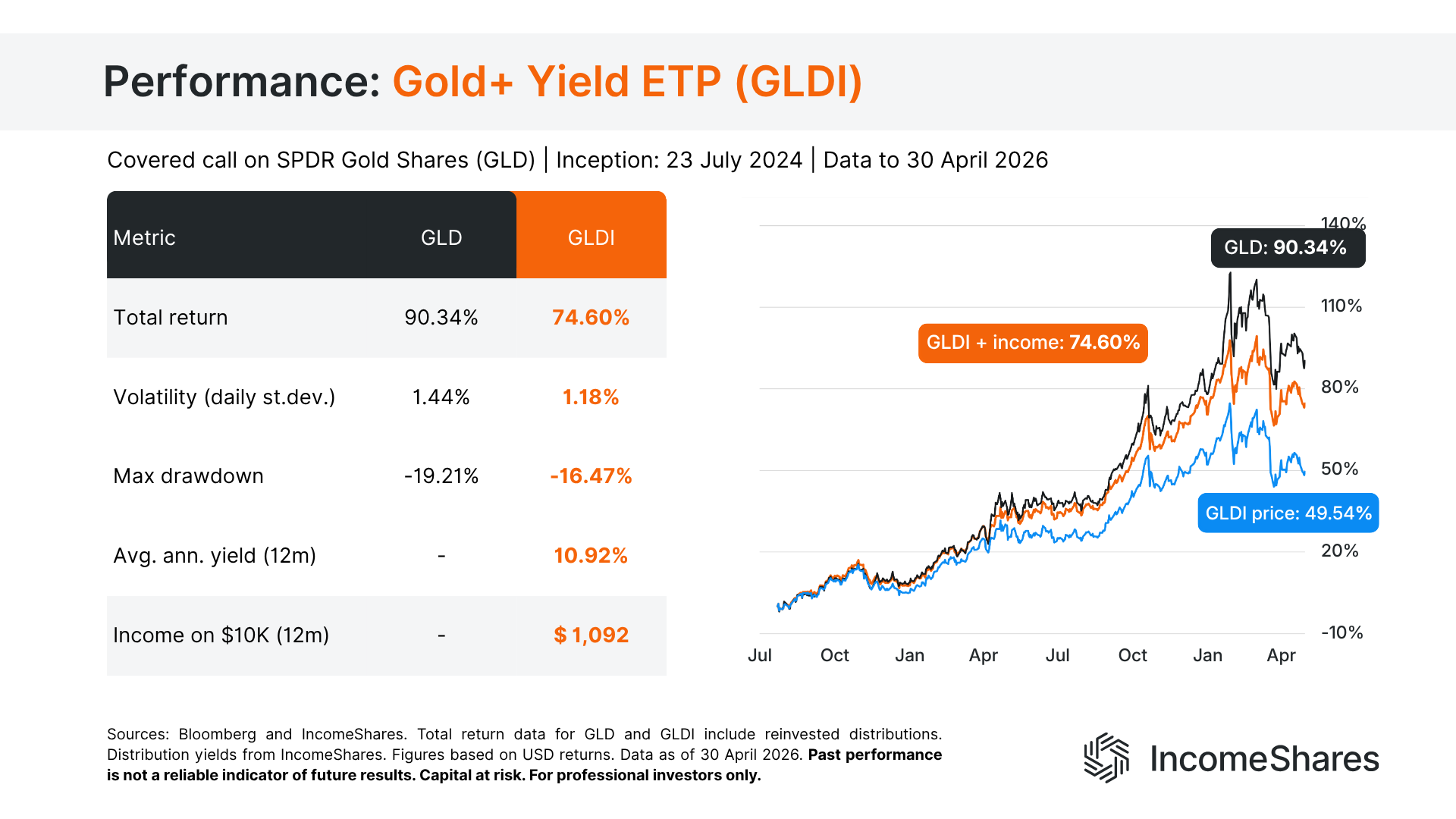

Take a model portfolio holding gold and long-dated US Treasuries. The IncomeShares Gold+ Yield ETP (GLDI) holds gold through SPDR Gold Shares (GLD) and sells call options on it. The IncomeShares 20+ Year Treasury Options ETP (TLTY) does the same with the iShares 20+ Year Treasury Bond ETF (TLT). Both could generate income within each bucket, while keeping exposure to the underlying asset’s price moves.

The results since launch show the potential trade-off. From 23 July 2024 to 30 April 2026, GLD returned 90.34% (black line, chart below). GLDI underperformed gold here – returning 74.60% with income reinvested (orange). Selling call options capped some upside as gold rallied. GLDI paid a 10.92% average annualised yield (while gold itself pays nothing). Note that GLDI produced a 49.54% “price only” return without the income component (blue).

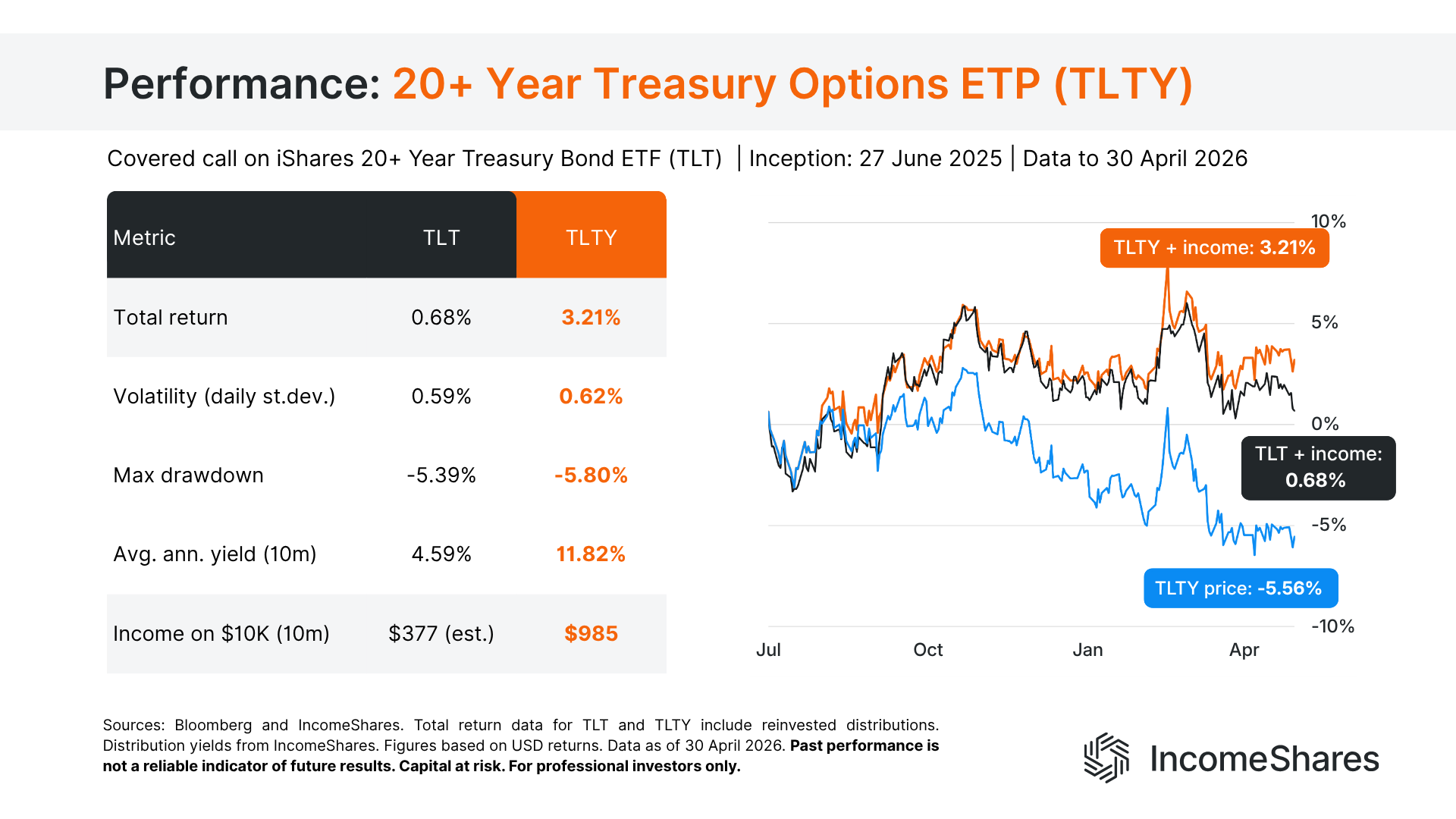

We launched TLTY in June 2025. Since then, TLT (black) returned just 0.68% with income reinvested, while TLTY (orange) returned 3.21%. In this case, the covered call strategy outperformed as TLT traded sideways. TLTY had an 11.82% average annualised yield against an estimated 4.59% from bond coupons alone. Without the income, TLTY’s price return was -5.56% (blue).

The same logic can apply to other underlying exposures within a model portfolio. Options income ETPs may give up some capital growth in exchange for higher income. In a flat or falling market, that income may improve the total return. In a strong rally, it might not.

Five things to weigh up before adding options income

1. The product wrapper: European model portfolios can hold UCITS funds for broader income exposures. But UCITS diversification rules prevent concentrated options strategies. For example, a covered call on a gold or bond ETF needs a non-UCITS ETP.

2. The allocation size: a T. Rowe Price study found that a 5% allocation to derivative income strategies could lower volatility across conservative, moderate, and moderately aggressive portfolios. The aim is to add a different source of income, not replace dividends and coupons altogether.

3. Income vs growth potential: options strategies tend to sacrifice upside potential for income. They may underperform the underlying asset on a total return basis.

4. Variable income: options premiums move with volatility, so income may vary month to month.

5. Tax treatment: options income ETPs may carry a tax edge over US dividend funds for EU and UK investors. We cover this in our article on US withholding tax.

Three things to remember

Income-focused model portfolios already spread income across several sources. Options income ETPs may add another source of income across multiple underlying asset classes.

A small allocation, around 5%, may add yield without reshaping a model portfolio.

UCITS portfolios can hold broad-index options income. Single-asset strategies and concentrated exposures may need a non-UCITS options income ETP.

Su capital está en riesgo si invierte. Podría perder toda su inversión. Por favor, consulte la advertencia de riesgos completa aquí.

Productos Relacionados:

Estrategia

Put garantizado con efectivo + Acciones

Rendimiento de

Distribución

39.29%

Estrategia

Covered Call

Rendimiento de

Distribución

11.96%

Estrategia

Basket of Income-generating ETPs

Rendimiento de

Distribución

37.34%

Estrategia

Covered Call

Rendimiento de

Distribución

12.45%

Estrategia

Estrategia de ingresos basada en opciones

Rendimiento de

Distribución

28.89%

Estrategia

Put garantizado con efectivo + Acciones

Rendimiento de

Distribución

32.86%