Autor

Jonathan Hobbs, CFA

Fecha

16 Jun 2026

Categoría

Education

Structured Notes vs Options Income ETPs

Su capital está en riesgo si invierte. Podría perder toda su inversión. Por favor, consulte la advertencia de riesgos completa aquí.

Structured notes and options income ETPs are different investment products. Yet many of them run on the same engine – selling options to earn income. This guide explains how structured notes work, including reverse convertibles and autocallables. It then shows how options income exchange-traded products could do a similar job, but in a different wrapper.

How do structured notes work?

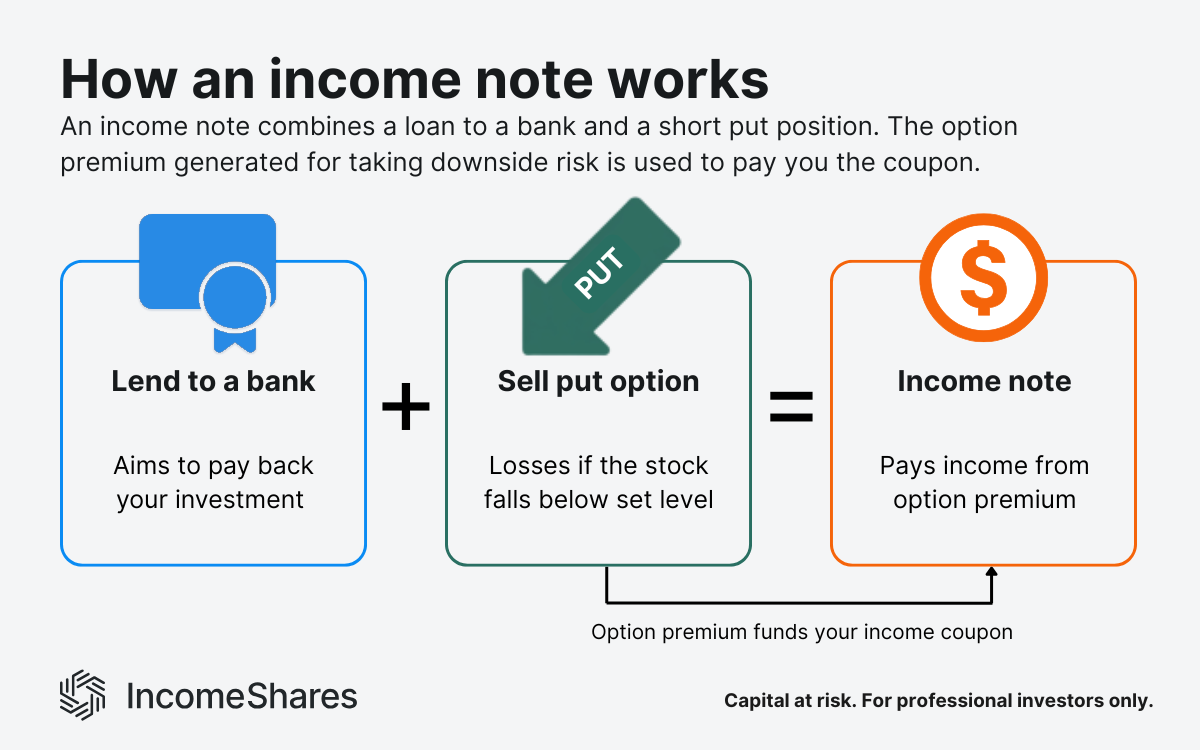

A structured note is essentially a loan to a bank, packaged as an investment you can buy. Banks issue them as debt securities, and institutional money managers and advisers typically buy them. Its payout depends on how an underlying asset – a stock, index, or commodity – performs.

Banks build structured notes for different goals: some for growth, some to protect capital, and some for income. This guide focuses on income notes – since these are the most similar to options income ETPs. Part of your money works like a normal loan, aiming to pay back what you put in. The rest goes into selling options, which generate the income you earn.

Structured notes and credit risk

You never own the stock or index itself. Instead, you hold the bank's promise to pay according to the note's terms. The bank sets those terms on the day you buy the note. They decide the income on offer (coupon) and the price level that would trigger a loss.

That promise is only as good as the bank behind it: if the bank goes under, you join the queue of creditors – no matter how well the underlying stock or asset performed. This is called credit risk, and it applies to every structured note.

Reverse convertible notes

The simplest income note is the reverse convertible. You lend the bank money and earn a high coupon. In return, you agree to buy a stock if it falls below a set level (called the barrier). Effectively, you've sold the bank a put option – the right to sell you that stock. The fee you earn for selling it (the premium) becomes your coupon.

The more the market expects the stock to swing in the future, the bigger the premium – so the higher the coupon potential. That expected swing is the stock's implied volatility, and it also increases the risk of a loss.

Hypothetical example: you buy a reverse convertible note that runs for one year and pays a 10% coupon. It's linked to a stock trading at $100, with a barrier at $70. What you get back depends on where the stock is trading after that year.

If the stock is above $70 after the year: you get your $100 back plus $10 of coupons. You get the income, and your capital back.

If the stock is below $70 after the year: you take the loss. You get shares worth less than you put in, with only the coupon to cushion it.

Autocallable notes

An autocallable note pays a coupon on set dates, as long as the asset stays above a set price. If the asset climbs back to its starting price on one of those dates, the bank “autocalls” the note. That means the note ends early – you get your money back plus the coupon, and the deal is done.

If the asset instead falls through a lower barrier (often 30–40% below its starting price), you take the loss when the note ends. An autocallable pays you for taking on the same risk as a reverse convertible note. You earn the coupon for accepting that the stock could fall – and cost you money.

Again, you've essentially sold a put option to the bank – the same mechanism behind the reverse convertible note.

Hypothetical example: you buy an autocallable note linked to a stock trading at $100. It pays an 8% coupon on set dates each year, with a barrier at $60.

If the stock is back at $100 on a set date: the note autocalls. You get your $100 back plus the 8% coupon, and it ends early.

If the stock is below $100 but above $60: you get the coupon, and the note runs on. Your $100 comes back later, provided the stock isn't below $60 when the note ends.

If the stock is below $60 when the note ends: you take the loss. You get shares worth less than $100, with the coupons as the only cushion.

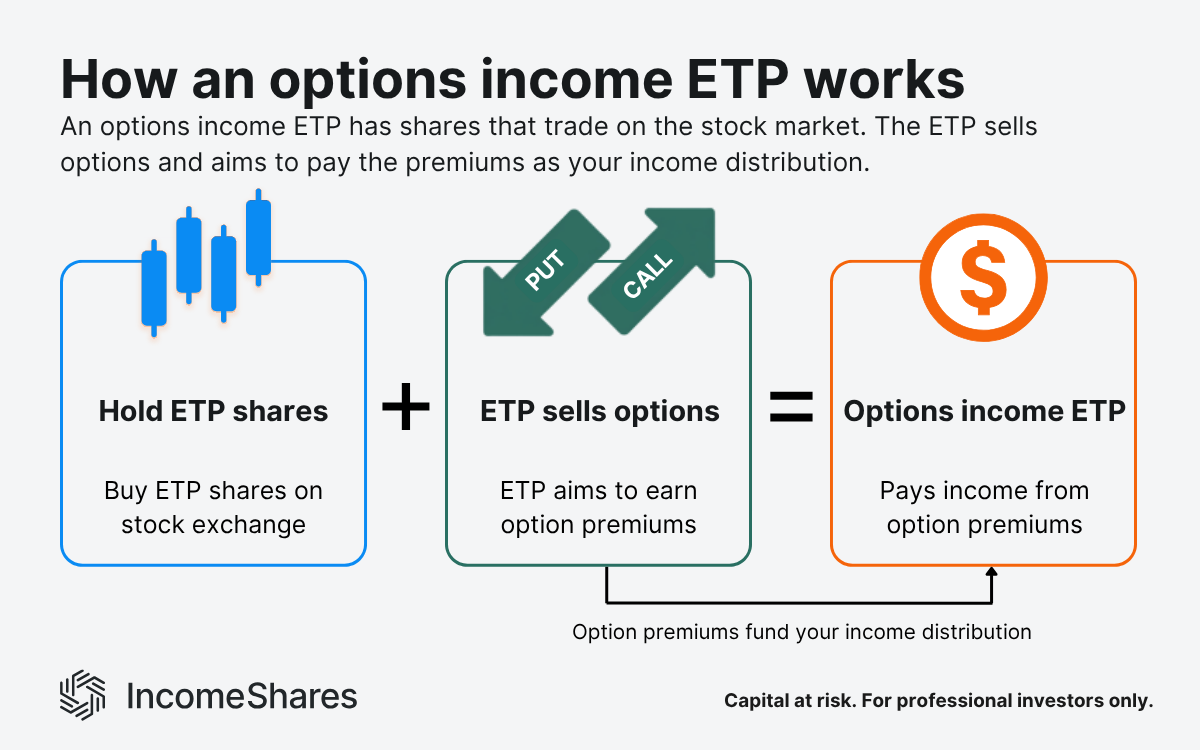

How IncomeShares ETPs compare with structured notes

IncomeShares exchange-traded products work on the same idea as an income note: they sell options and pay out the premium as income. The main difference is the wrapper. An IncomeShares ETP is a fund-style product you can buy and sell on the stock market. It sells options on an asset it holds, like a stock, index, or commodity.

That shared idea is where the similarity ends. Four things set them apart:

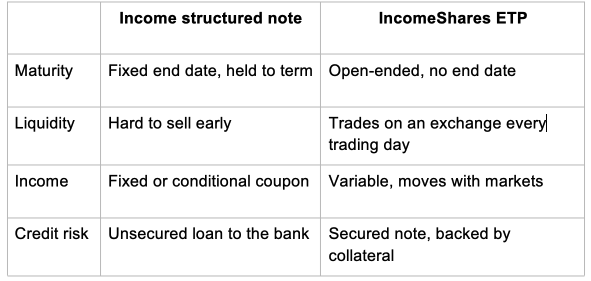

An income note ties your money up until its end date, and selling early is difficult. An IncomeShares ETP trades through the day, so you can buy or sell at the market price, subject to market liquidity.

A note's coupon is set in advance. An IncomeShares ETP's income floats with option premiums – less predictable, but it can rise when volatility climbs.

Unlike a note, IncomeShares ETPs own real assets that your investment is entitled to. The ETP holds these separately from the issuer. So you're not relying on the bank's promise alone. That may reduce credit risk, but it doesn't remove it.

Three things to remember

There are several types of structured notes. Some aim for growth, some protect your capital, and some pay income.

An income note pays a coupon because you've effectively sold a put option to the bank. You earn it for taking on the risk that the stock falls.

IncomeShares ETPs earn income the same way, but in a different wrapper. They trade every day and hold real assets behind them, instead of relying on a bank's promise.

Su capital está en riesgo si invierte. Podría perder toda su inversión. Por favor, consulte la advertencia de riesgos completa aquí.

Productos Relacionados:

Estrategia

Put garantizado con efectivo + Acciones

Rendimiento de

Distribución

63.28%

Estrategia

Covered Call

Rendimiento de

Distribución

11.92%

Estrategia

Covered Call

Rendimiento de

Distribución

12.62%

Estrategia

Covered Call

Rendimiento de

Distribución

11.98%

Estrategia

Estrategia de ingresos basada en opciones

Rendimiento de

Distribución

29.28%

Estrategia

Cartera de Estrategias de Ingresos Multi-Activo

Rendimiento de

Distribución

57.94%