Author

Jonathan Hobbs, CFA

Date

09 Jun 2026

Category

Education

ISA vs SIPP for Options Income ETPs

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

UK investors can hold options income exchange-traded products (ETPs) in two main tax-efficient wrappers. One is the stocks and shares ISA, and the other is the self-invested personal pension (SIPP). Each wrapper can shelter any options income and ETP capital gains from tax – they just do it at different times. Here's how the two compare.

Why options income ETPs could make sense in a tax-efficient wrapper

Options income ETPs aim to pay income to investors each month. They typically hold shares in stocks or other assets, and sell options on those shares.

For example, the IncomeShares Magnificent 7 Options ETP (MAGO) holds around 25% in Magnificent 7 shares (capital gains potential). It uses the rest to sell put options on those stocks, which can earn premiums (income potential).

So, an investor holding this type of product may owe income tax on the monthly distributions. They could also owe capital gains tax on any growth in the ETP share price when they sell. A tax-efficient wrapper could change that.

Some investors reinvest the income back into the ETPs instead of taking it out. Reinvested income can potentially compound over time. In a tax-efficient wrapper, it can compound without being taxed along the way.

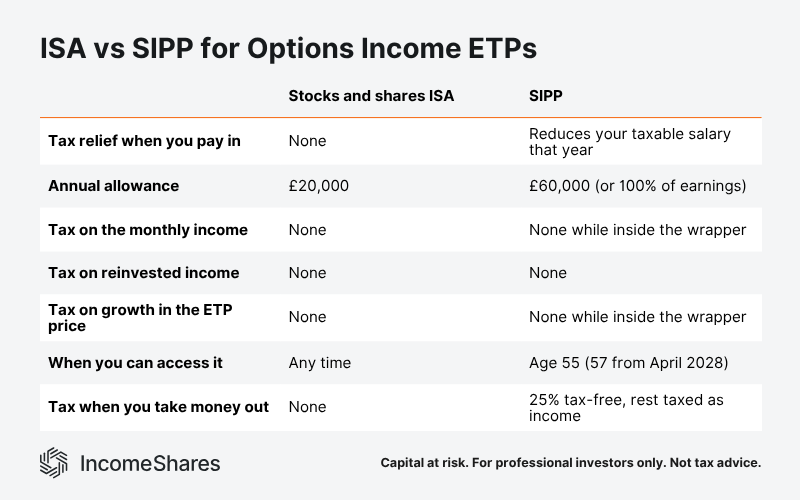

An ISA saves you tax later

An ISA doesn’t give you any tax breaks when you pay money into it. You fund it with money you've already been taxed on – like income from your job. You can currently add up to £20,000 each tax year (April to April).

The potential tax savings come later. While your money stays inside the ISA, any income or gains are completely tax-free. That’s true regardless of your investment strategy – whether buying and holding, or actively trading. And when you take money out of an ISA, you don’t pay any tax on it either.

Hypothetical example: Alice invests £10,000 into a stocks and shares ISA from her salary (which she already paid 40% tax on). Alice pays her tax upfront. She then buys an options income ETP within her ISA. After that, she pays no more tax. No income tax, no capital gains tax, and no tax when she takes her money out of the ISA.

A SIPP saves you tax upfront

A SIPP works the other way round. What you pay in reduces your taxable salary upfront (and hence your income tax bill for that year). You can currently add up to £60,000 a year into your SIPP, or 100% of your earnings if that's lower. Inside the wrapper, it works the same as an ISA: any income or capital gains are tax free.

The tax comes later, when you decide to take money out of your SIPP. A SIPP locks your money until age 55 (rising to 57 from April 2028). You can then take 25% of your pension pot out tax-free. But you’ll need to pay regular income tax on the rest at your normal tax rate.

Hypothetical example: Bob pays £10,000 into a SIPP, which reduces his taxable salary and saves him £4,000 in income tax that year. So Bob cuts his tax bill upfront. He then buys an options income ETP within his SIPP. His income and any growth are tax-free inside the SIPP, just like with Alice's ISA. The tax comes later for Bob, when he takes his money out for retirement. At that point, he can take 25% out tax-free, but will need to pay regular income tax on the rest.

IncomeShares ETPs may be eligible to hold in a stocks and shares ISA or SIPP, subject to broker availability. Tax rules depend on your circumstances and may change.

Three things to remember

An ISA can save you tax later. You pay in from taxed income, but any income, gains, and withdrawals are tax-free, any time.

A SIPP can save you tax upfront. It cuts your tax bill now, but locks your money until 55 (57 from 2028) and taxes most withdrawals.

Inside either wrapper, any income and gains are tax-free. The wrapper changes when you're taxed, not whether you're taxed.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategie

Covered Call

Ausschüttungsrendite

12.10%

Strategie

Basket of Income-generating ETPs

Ausschüttungsrendite

39.99%

Strategie

Covered Call

Ausschüttungsrendite

12.63%

Strategie

Optionsbasierte Einkommensstrategie

Ausschüttungsrendite

29.30%

Strategie

Optionsbasierte Einkommensstrategie

Ausschüttungsrendite

59.25%