Author

Jonathan Hobbs, CFA

Date

30 Jan 2025

Category

Martket Insights

How 0DTE Cash-Secured Put Strategy ETPs Perform in Different Markets

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Some Cash-secured put Exchange-Traded Products (ETPs) use0DTE (zero days to expiration) optionsto generate income. The strategy involves selling put options that expire on the same day – and holding enough cash to buy the underlying asset (e.g., an index or a stock) if needed. This guide compares how these ETPs might perform in bull, bear, and sideways markets.

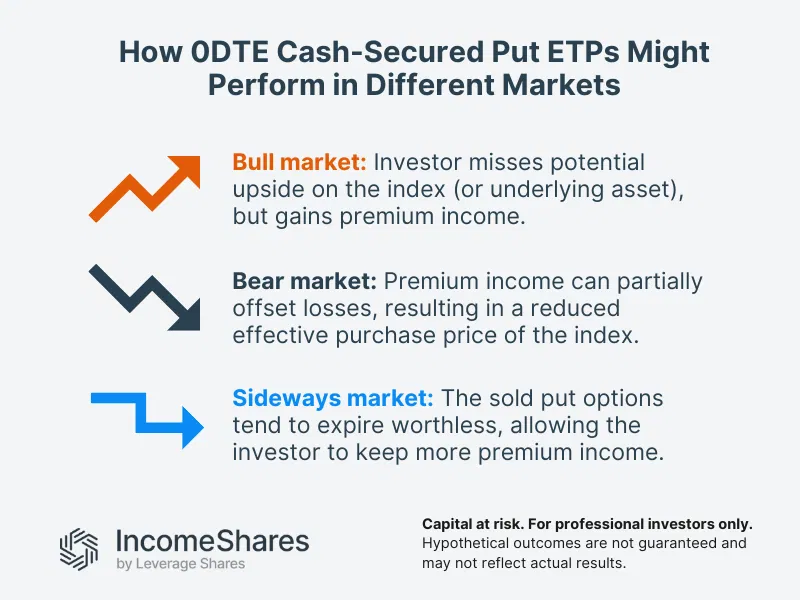

Performance in bull markets

In bull markets, prices trend higher. For cash-secured put ETPs, this environment presents a potential tradeoff for the investor.

High income potential: Rising prices tend to favour put option sellers. With rising prices, there’s less chance that put option buyers will end the trading day “in the money” (ITM). In other words, they’re less likely to put (sell) the index (or underlying asset) to the ETP at the higher strike price. That means the ETP doesn’t have to buy the index for more than it’s worth. It can potentially keep its full premium as income.

Missed market gains: Since puts tend to expire worthless in rising markets, the ETP can keep more of the premium as income. But without owning the index (or underlying asset), the ETP misses out on any potential gains from rising prices.

And that’s the trade-off in a bull market for cash-secured put ETPs: sacrificing growth potential for income.

Performance in bear markets

Bear markets (where prices drop) can be challenging for cash-secured put ETPs, but they can also have some potential benefits.

Higher premium income potential: As the market falls, the demand for puts generally rises because investors look for downside protection. This increased demand can drive up put premiums, which can boost the income generated by the ETP (from selling puts).

Partial loss offset: If prices fall below the put option strike price, the ETP may need to buy the underlying asset at the strike price. Here, the premium income can partially offset the loss: it can reduce the effective purchase price of the stock.

In down markets, cash-secured put ETPs may have smaller losses compared to owning the underlying asset outright. But the strategy won’t eliminate risk – losses can still be large if markets drop sharply.

Performance in sideways markets

Sideways or range-bound markets can be an ideal environment for cash-secured put ETPs:

Steady income: The ETP can collect premiums from selling put options, even if the market doesn’t move much. In flat or choppy markets, the put options sold can also expire worthless, so the ETP doesn’t need to buy the underlying stock or asset.

Outperformance potential: In flat markets, the ETP can outperform simply by generating consistent income. Meanwhile, the underlying stock or asset stays range-bound.

Overall, sideways markets maximize income potential while keeping risk relatively low.

Key takeaways

In rising markets, cash-secured put ETPs can benefit from collecting premiums when puts expire worthless.

In bear markets, premium income can offset some losses, but the strategy doesn’t remove risk.

Sideways markets are typically ideal for cash-secured put ETPs. They can potentially generate steady income without exposure to large price swings.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Cash-Secured Put + Equity

Distribution Yield

73.32%

Strategy

Cash-Secured Put + Equity

Distribution Yield

39.97%