Author

Jonathan Hobbs, CFA

Date

05 Nov 2024

Category

Martket Insights

0DTE Options Explained: How They Work In Trading

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Zero Days to Expiration (0DTE) options are options that expire the same day they are traded. They are designed for traders looking to take positions on short-term market movements.

What Are 0DTE Options?

Unlike regular call or put options, 0DTE options are contracts with less than one day until expiration. You often see them in major stock indices like the S&P 500 (SPX) or in highly traded stocks.

0DTE call option: The buyer gets the option (but not the obligation) to buy an asset (like a stock or index) at a set price – before the option expires at the end of the trading day.

0DTE put option: The buyer gets the option (but not the obligation) to sell an asset at a set price – again, before the option expires at the end of the trading day.

These options tend to be highly speculative because of their short-term nature, but they can also help manage risk in certain situations (more on that later).

The Role of Time Value in 0DTE Options vs. Regular Options

Regular options have something called time value, which means part of their price comes from the extra time left until they expire. The more time an option has before it expires, the more chance the market price can move in a way that makes the option profitable. But as the expiration approaches, time value drops since there’s less chance for the market to move in your favor.

But with 0DTE options, there’s almost no time value left because they expire the same day. Instead, their value is mostly based on intrinsic value – i.e., how close the current market price is to the strike price. This makes 0DTE options highly sensitive to market movements throughout the day.

Why Use 0DTE Options?

Investors use 0DTE options for three main reasons:

Speculation: Trying to profit from short-term market swings. For example, you buy an 0DTE call option because you think the price of an investment will go up today.

Hedging: Protecting against sudden market drops. For example, if you’re worried about a market crash today, you might buy a 0DTE put option to cover your downside risk. If the asset drops, you get to sell that asset to the put option buyer at the higher strike price.

Income generation: Some traders sell 0DTE options to earn a premium (the upfront fee from selling an option). You’re betting that the market won’t move against you during the day, so the option expires worthless. If that happens, the premium becomes pure profit.

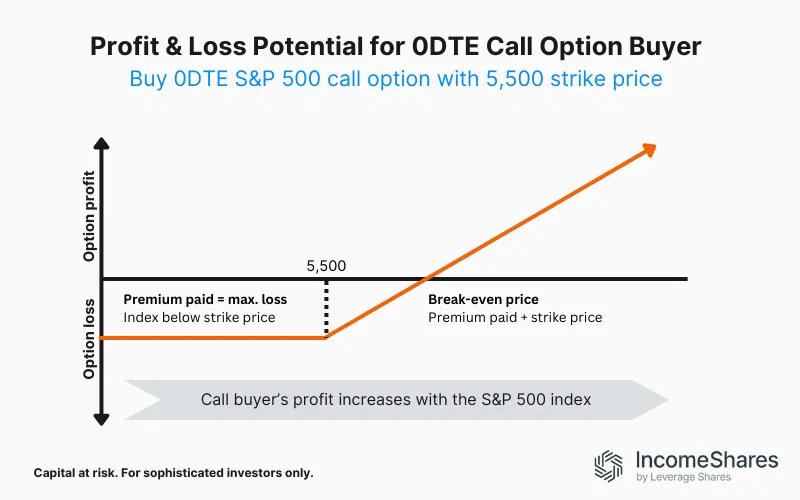

Example 1: Buying a 0DTE Call Option

It’s 10 AM and you expect the S&P 500 to rise throughout the day. You buy a 0DTE call option with a strike price of 5,500. If the S&P 500 rises above 5,500 by the market close, you have two choices:

Sell the call option to another trader for a quick profit, without having to buy the S&P 500 itself.

Exercise the option to buy the S&P 500 at the strike price of 5,500 (if you want to own the index).

Since 0DTE options have such a short time frame, most traders prefer to sell the option and lock in their gains rather than exercising it to buy the index.

If the S&P 500 drops instead, the call option becomes worthless. In that case, you lose the upfront premium you paid for it.

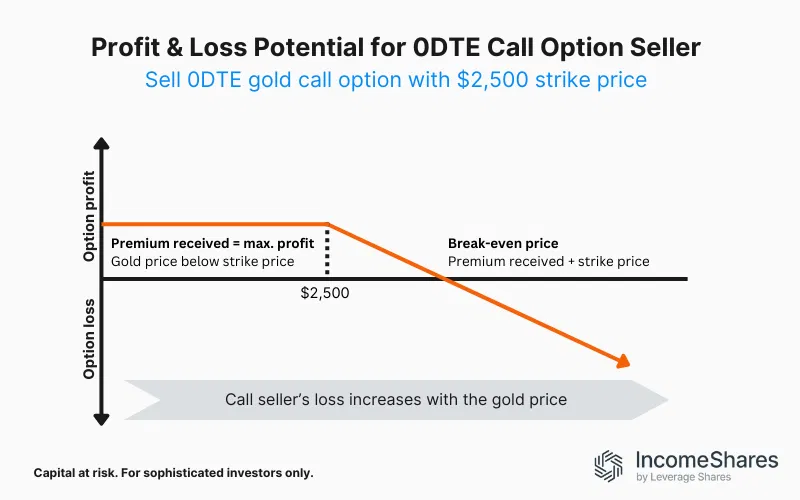

Example 2: Selling a 0DTE Call Option on Gold

It’s mid-morning and you believe gold prices won’t rise much for the rest of the day. You sell a 0DTE call option with a strike price of $2.500 and collect a premium upfront for selling the option. And you’re obligated to sell gold at $2,500 if the buyer exercises the option.

Profit scenario: If gold stays below $2,500, the option expires worthless, and you keep the entire premium.

Loss scenario: If gold rises above $2,500, you may need to sell gold to the option buyer at $2,500, which could result in a loss.

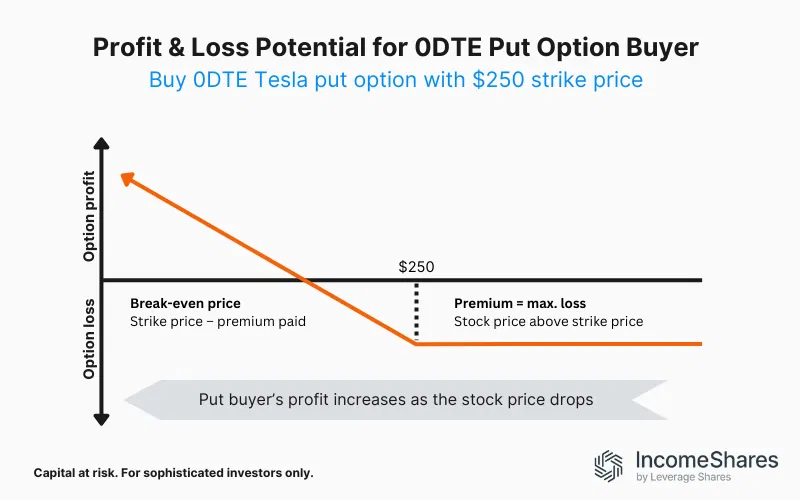

Example 3: Buying a 0DTE Put Option on Tesla

It’s noon, and you think Tesla’s stock will drop before the end of the trading day. You buy a 0DTE put option with a strike price of $250. If Tesla drops below $250, you can sell the option for a profit or exercise it to sell the stock at the strike price.

Profit scenario: If Tesla falls to $240, you can sell the put option for a profit.

Loss scenario: If Tesla stays above $250, the option expires worthless, and you lose the premium paid.

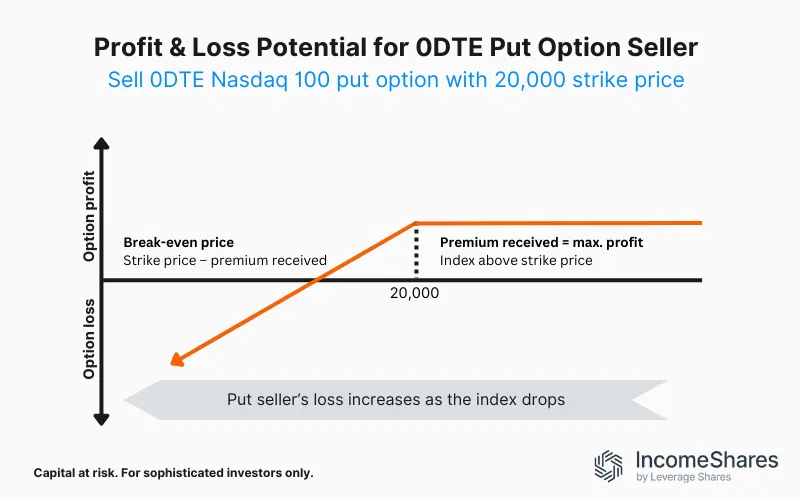

Example 4: Selling a 0DTE Put Option on the Nasdaq 100

You believe the Nasdaq 100 won’t drop much during the day. So, you sell a 0DTE put option with a strike price of 20,000. By selling the option, you collect the premium upfront. But you’re obligated to buy the index at 20,000 if the buyer exercises the option.

Profit scenario: If the Nasdaq 100 stays above 20,000, the option expires worthless, and you keep the premium as profit.

Loss scenario: If the Nasdaq 100 falls below 20,000, you may have to buy the index at the strike price. That could result in a loss.

At IncomeShares, we use 0TDE options in some of our income generating ETP (exchange-traded product) strategies. Learn more about our range of ETP products here.

Key Takeaways

0DTE options are options that expire on the same day. You’ll often see them with big indices like the S&P 500 or highly traded stocks.

Traders use 0DTE options to make quick bets on market moves. They can also use them to hedge against sudden drops, or earn income by collecting premiums.

0DTE options can be risky because of the short time frame. This makes them best suited for traders who can act quickly and manage risks.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Cash-Secured Put + Equity

Distribution Yield

47.52%

Strategy

Cash-Secured Put + Equity

Distribution Yield

73.32%

Strategy

Cash-Secured Put + Equity

Distribution Yield

39.97%