Author

Jonathan Hobbs, CFA

Date

06 Nov 2024

Category

Martket Insights

NAV Erosion Explained: Why It Matters In Options ETPs

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

When investing in options ETPs (exchange-traded products), you may come across the term NAV erosion. But what is it, and why should it concern income investors? This guide will break down NAV erosion, how it happens, and ways to mitigate it.

What is NAV erosion?

NAV stands for the “net asset value” of a fund. It represents the total value of the fund’s assets minus its liabilities and operating costs. In other words, the NAV is what’s left for the fund’s investors.

For ETPs, the NAV per share is like the product’s “price tag” – showing the proportionate NAV value for each individual share.

When we talk about NAV erosion, we mean that the value of the ETP’s assets is gradually shrinking over time. This can happen in products that pay out regular income to investors in the form of options premiums.

For example, in a covered call strategy, the ETP sells calls to earn income (yield) for investors. And in an 0DTE put-write strategy, the ETP sells puts.

Why do NAVs erode with ETPs that sell options?

ETPs that generate income through strategies like selling options usually pay out that income to investors. In other words, that yield is subtracted from the NAV.

While this can give you a steady cash flow, it can also eat away at the fund’s underlying asset value, causing NAV erosion. Here’s why:

Regular payouts: These products regularly distribute income to investors. But if the fund’s assets aren’t growing fast enough to replace what’s being paid out, the NAV slowly drops.

Limited upside: In strategies like covered calls, the ETP gives up some potential gains on the underlying asset. So if the market goes up, the ETP’s NAV doesn’t always go up as much, giving it less room to grow.

Declining asset value: When the value of ETP assets drop (like in a stock market dip), the NAV falls, too. Combine this with regular yield payouts, and the NAV can erode fast.

Why should you care about NAV erosion?

It’s nice to earn regular income – especially if the yields are high. But as an investor, you should also factor potential NAV erosion into your long-term returns. Over time, the ETP might have fewer assets generating income, which could mean:

Lower future income: As the NAV drops, the ETP has fewer assets left to sell options on or collect premiums from, leading to smaller payouts.

Capital loss: If you plan to sell your shares in the ETP, a lower NAV means your investment may be worth less than what you initially put in.

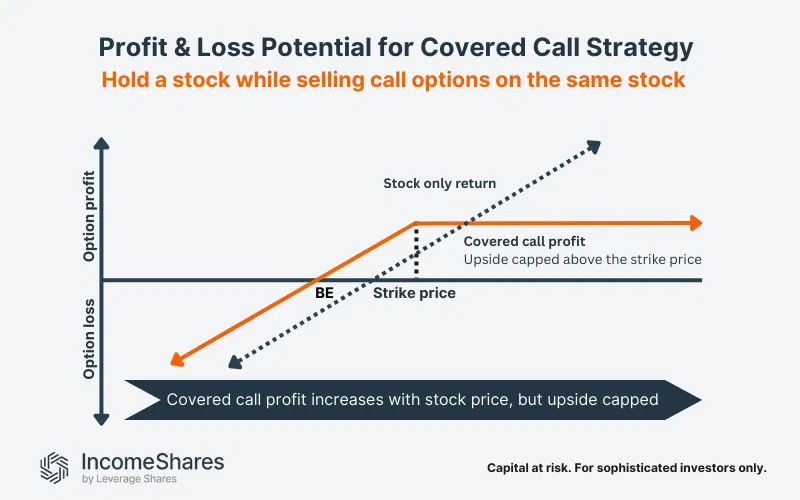

Example: Covered call ETP strategy

A covered call ETP pays a high yield to investors each month by selling call options on a stock while holding the stock itself.

If the stock price stays below the strike price, the option expires worthless. The ETP keeps the premium – paying it as income to investors.

If the stock price rises above the strike price, the ETP sells the stock at the strike price, missing out on further gains. Over time, if the payouts consistently exceed the stock’s growth, this can lead to NAV erosion.

If the stock price keeps falling, the income from the option premiums might not be enough to offset the losses in the stock’s value. This could accelerate NAV erosion.

How can options ETPs reduce NAV erosion?

When it comes to investing, you can rarely have your cake and eat it. But there are a few ways for ETPs to reduce NAV erosion.

Active management: One way to mitigate NAV erosion is through active management. This involves continuously adjusting the options strategy based on market conditions. For example, fund managers might target higher yields during stable markets and focus on protecting the NAV when volatility spikes. At IncomeShares, we actively manage our ETPs’ options strategies to try and adapt to these changes.

Managing yield payouts: High yields might sound great, but they can eat into the NAV over time if the fund is paying out more than it’s bringing in. By keeping the yield payouts at more sustainable levels, ETPs can avoid draining their NAV. This can keep the fund more stable in the long run.

Keeping cash on-hand: In our IncomeShares 0DTE put-write strategy, we hold cash to cover potential put option exercises. This way, if the market moves against us, we can buy the underlying asset without taking on excessive risk. This helps protect the NAV from sharp drops during volatile periods, while still generating income from option premiums.

Key takeaways:

NAV erosion happens when ETPs pay out more income than they can replenish through asset growth.

It’s a risk in high-yield ETPs using strategies like covered calls and put-write options, where upside potential is limited.

Active management can help reduce the risk of NAV erosion by adjusting strategies in real-time based on market conditions.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Cash-Secured Put + Equity

Distribution Yield

62.66%

Strategy

Cash-Secured Put + Equity

Distribution Yield

40.06%

Strategy

Cash-Secured Put + Equity

Distribution Yield

37.51%

Strategy

Cash-Secured Put + Equity

Distribution Yield

47.45%

Strategy

Covered Call

Distribution Yield

12.08%