Author

Jonathan Hobbs, CFA

Date

07 Feb 2025

Category

Market Insights

American vs European Options: What’s the Difference?

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Options trading comes with many moving parts, but one fundamental distinction is whether an option is American-style or European-style. This guide will compare American vs European options and explain how they differ.

Key differences: American vs European options

Options give the buyer certain exercise rights. For example, a call option buyer has the right to buy the underlying stock (or asset) at a preset strike price. A put option buyer, on the other hand, has the right to sell a stock at the strike price.

When it comes to those exercise rights:

American options: can be exercised anytime before the expiration date.

European options: can only be exercised on the expiration date.

This impacts pricing, risk management, and trading strategies – especially for options-based Exchange-Traded Products (ETPs).

The table below outlines a few more differences between European and American options.

Example: American-style call option on Nvidia (NVDA)

An investor buys a call option on Nvidia stock (NVDA) with a $125strike price. The call option expires in one month. Since Nvidia is a US-listed stock, its options are American-style. That means the investor can exercise the option to buy the stock before expiration (if NVDA trades above the $125 strike price).

If Nvidia stock rises to $135, the investor can exercise the option early. They can buy the stock at $125and profit from the difference.

But if the stock price stays below $125, the option expires worthless. And the investor loses the premium paid.

Note: the hockey-stick diagrams for American options look the same as they do for European options. The chart only shows the profit or loss at expiration – regardless of whether the option allows early exercise.

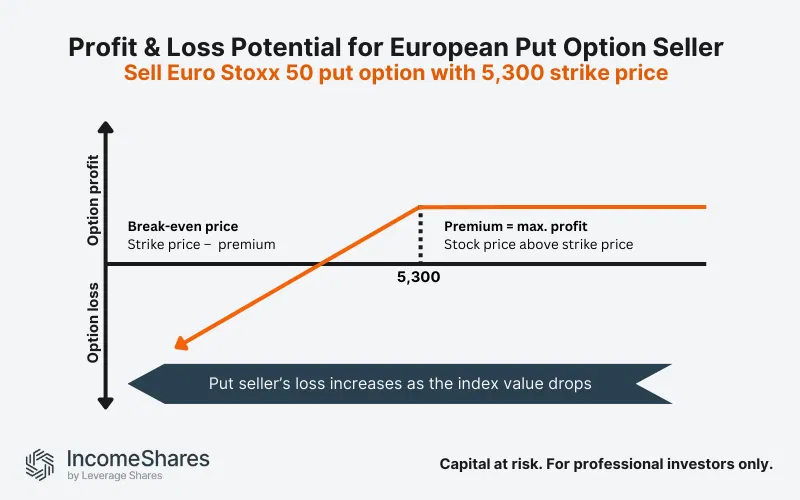

Example: Sell European-style put option on the Euro Stoxx 50 Index

A trader sells a put option on the Euro Stoxx 50 Index with a 5,300 strike price. The option expires in one month. Since Euro Stoxx 50 options are European-style, the option buyer can’t exercise early. They can only exercise the option to sell the index at expiration.

If the index falls to 5,000 at expiration, the option buyer can exercise the put option. Therefore, the trader must buy at 5,300 – and realize a loss.

But if the index stays above 5,300, the option expires worthless. The trader (option seller) keeps the premium received as profit.

American vs European options and pricing

American-style options generally have a higher premium than European options. The option holder is typically willing to pay more for the flexibility of early exercise.

The Black-Scholes model – a key formula for pricing European options – assumes no early exercise. For American options, traders often use modified models to account for early exercise risk.

The put-call parity formula helps explain fair value relationships between calls, puts, and the underlying stock. But for American options, early exercise rights can cause deviations from put-call parity.

Options Greeks & early exercise

Early exercise is often influenced by the options “Greeks” – especially theta (time decay) and delta (price sensitivity).

For example:

High theta near expiration could encourage early exercise for American-style options.

Dividend payments may cause call option holders to exercise early to capture the dividend.

What options style does IncomeShares use?

Since IncomeShares’ options ETPs are based on US-listed stocks, ETFs, and indices, they use American-style options.

That means:

Covered call ETPs could see early assignment (i.e. forced stock selling) risk if the stock price moves sharply.

0DTE put-wrting ETPs could face early exercise if deep in the money before expiration. But since 0DTE put options expire the same day, early exercise is rare.

Key takeaways

American options can be exercised anytime before expiration, while European options can only be exercised at expiration.

Most US-listed stock and ETF options are American-style, while some European index options are European-style.

Put-call parity and options pricing models work differently for American vs European options. Early exercise rights of American options tend to complicate option valuation models.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Cash-Secured Put + Equity

Distribution Yield

45.06%

Strategy

Cash-Secured Put + Equity

Distribution Yield

55.09%

Strategy

Cash-Secured Put + Equity

Distribution Yield

65.05%

Strategy

Cash-Secured Put + Equity

Distribution Yield

46.84%

Strategy

Cash-Secured Put + Equity

Distribution Yield

58.93%