Author

Violeta Todorova

Date

12 Nov 2025

Category

Market Insights

Can the Magnificent Seven Keep Driving the Market Higher?

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Key Takeaways

Market leadership remains narrow, with the Magnificent Seven driving most of the S&P 500’s gains.

AI-linked capex remains strong but is facing increasing investor scrutiny around returns.

The lofty valuations of mega-caps amplify the impact of any earnings disappointments.

Corporate Earnings Continue to Drive Markets

With earnings season winding down, around 82% of companies have beaten profit forecasts. More than 450 S&P 500 companies have now reported third-quarter earnings, covering roughly 80% of the index by market capitalization. Earnings growth is tracking at 14.6% year-on-year, almost double the 7.4% expected at the start of the reporting season.

This strength is encouraging us to lift our outlook, with the S&P 500 likely to reach 7,000 by year end and 7,600 by the end of 2026, driven mainly by earnings growth. Earnings breadth is improving, meaning more sectors are contributing to profit gains instead of just a few large tech names.

The results so far confirm that corporate America is still expanding, though with clear divergence between sectors. The biggest companies in technology and AI continue to post record profits, while smaller firms in consumer-facing industries are showing more stress.

Volatility Signals Cautious Optimism

Current volatility patterns point to a jittery rally rather than a calm, confident one. The VIX, which tracks expected stock market swings, is holding above last year’s lows and tends to bottom higher around 16 to 17. There are also more days when both the S&P 500 and the VIX rise together, a sign that traders are buying call options to join the rally while also paying for puts to protect against a sudden drop. This mix of buying and hedging suggests investors still believe the uptrend can continue yet remain wary of potential setbacks.

AI Capex Surge Faces Rising Investor Scrutiny

AI infrastructure spending remains the defining theme of this market cycle. Yet while investment remains strong, investors are becoming more selective and focused on measurable returns rather than headline spending.

This earnings season has shown that investors are growing less forgiving. With valuations stretched and momentum concentrated in a few mega-caps, companies that merely met expectations are being sold off, while those delivering strong beats are rewarded only modestly.

Credit markets are reinforcing this theme. New issuance among large tech companies has led to wider spreads, suggesting investors are growing wary of peak spending and stretched valuations.

AI Spending and Chip Production Expand

Last week’s AI stock selloff may have shaken confidence, but the underlying spending cycle continues to expand. Nvidia’s chief executive Jensen Huang told reporters in Taiwan that demand is rising every month and that he asked TSMC for more wafer capacity. Memory suppliers Samsung, SK Hynix, and Micron are all ramping up output to support AI chip production.

TSMC reported slower monthly revenue growth, showing how tight capacity has become even as orders stay strong. Qualcomm’s CEO also said that global demand for AI chips is being underestimated, reinforcing that the long-term story remains intact.

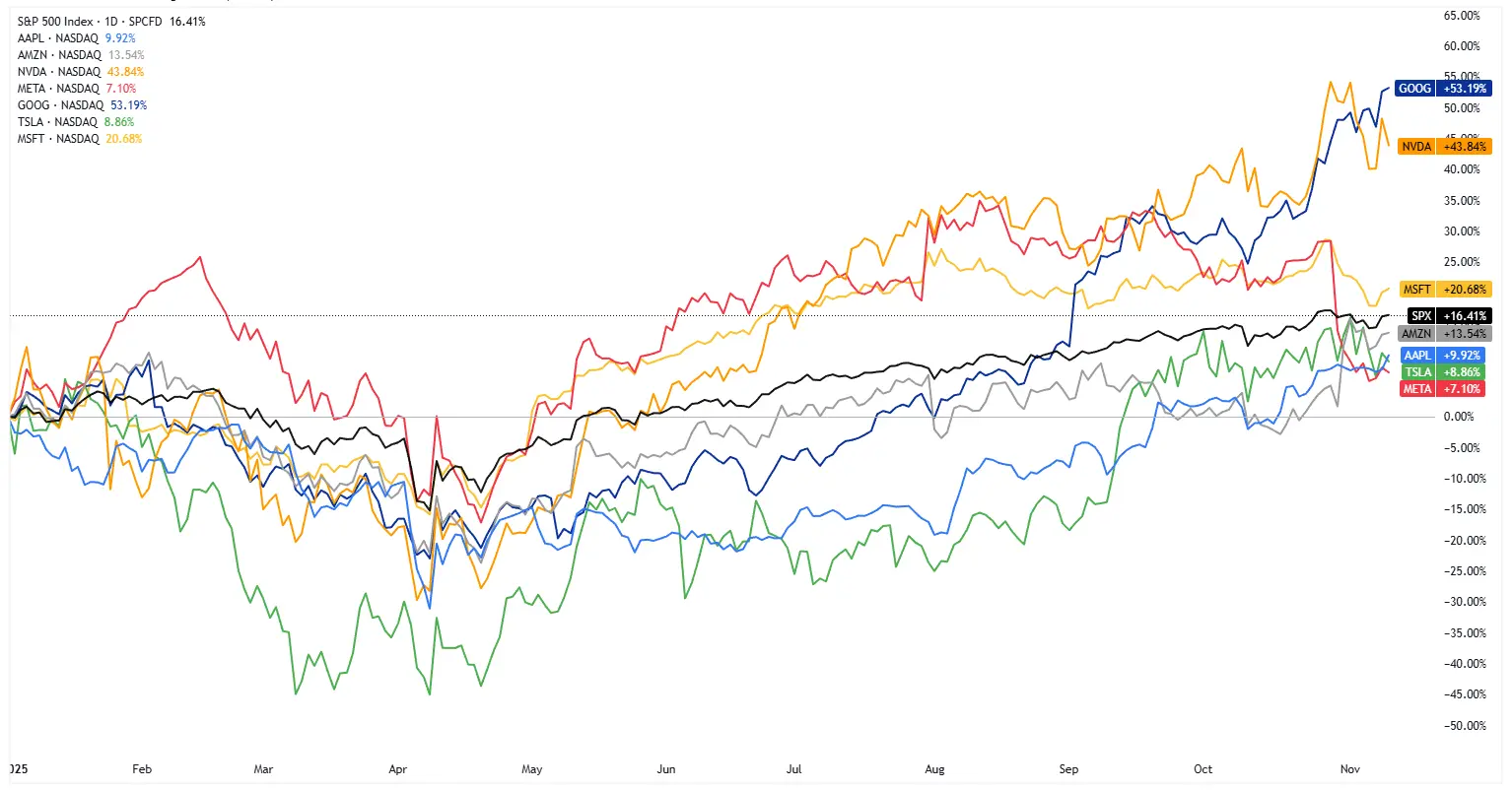

S&P 500 Shows Narrow Market Leadership

The S&P 500 has rose 2.2% in October and despite last week’s volatility, the index remains more than 9% above its 200-day moving average. Only around 40% of index members trade above their 50-day moving averages, and the percentage above their 200-day average is at the lowest point since June. Without contributions from the Magnificent Seven, the S&P 500 would have finished October in negative territory.

This widening gap between market leaders and laggards highlights a growing imbalance. The forward P/E ratio of 22.88 sits near its pandemic-era peak, and the valuation spread between the largest tech names and the rest of the market is at a record high.

Market breadth improved last Friday, with 394 stocks in the S&P 500 advancing. That shows buyers are still stepping in, though fewer are willing to chase prices at the top.

October Trading Volume Hits Record Levels

October also saw average daily trading volume reach a record 20.6 billion shares, much of which was concentrated in speculative names outside the benchmark. Institutional and retail activity surged, but the underlying picture still reflects a narrowing rally rather than a broad one.

At the same time, active mutual funds have trimmed their exposure to large-cap tech stocks, cutting their tech weighting to around 30%. That’s the biggest underweight in five years and highlights growing caution around valuations after a prolonged AI-driven rally.

Tech Volatility Returns as AI Trades Unwind

U.S. equities are attempting to regain their footing after a sharp selloff last week that hit some of the market’s most crowded trades. Technology stocks bore the brunt of the decline, with semiconductors and AI-linked names experiencing their worst weekly performance since April. The turbulence reignited a critical question for investors: Can the so called Magnificent Seven, which are the dominant force behind this cycle’s returns continue to steer markets higher? Wall Street’s gaze remains fixed on these mega-caps, whose combined weight is a quarter of the S&P 500 and still defines market direction. Investors are trying to reassess just how much gas is left in the mega-cap engine that has powered the U.S. market’s record run this year.

Will Market Leadership Broaden Beyond Mega-Caps?

A central question for portfolio managers is whether leadership can rotate away from mega-cap tech. We expect concentration to persist through year-end. The market-weighted S&P 500 continues to outperform the equal-weighted index by more than 8% year-to-date, extending a trend that began in 2023. For this to change, small- and mid-cap earnings need to show sustained improvement, something not seen since mid-2022, but likely to emerge in the U.S. in 2026 as more rate cuts from the Fed are delivered.

Until that change occurs, mega-caps retain a clear relative advantage. Their balance sheets, scale, and dominant positions in monetizable AI infrastructure allow them to maintain premium valuations despite rising scrutiny.

Market Outlook: Strong Yet Fragile Rally

In the near term, the Magnificent Seven appear capable of continuing to support headline index gains. AI-driven investment remains strong, mega-cap fundamentals are resilient, and fund flows continue to favour the sector. Yet risks are rising. Market breadth remains thin, valuations are elevated, and investors are increasingly intolerant of earnings results that merely meet expectations.

The rally can continue, but its foundation is becoming increasingly narrow. While the AI cycle remains structurally intact, the concentration of returns among a few companies leaves markets vulnerable to sudden shifts in sentiment. A more durable advance will require broader corporate participation, particularly from small- and mid-cap companies.

Conclusion:

The market’s heavy reliance on the Magnificent Seven has created an environment where stretched valuations, particularly within Big Tech, pose a growing risk. While an eventual repricing may unfold slowly or suddenly, the vulnerability is increasingly evident. Several of these mega-cap names trade far above the market’s historical valuation range, with Nvidia standing out after extreme price swings and a premium multiple that leaves little margin for error. Even within the group, valuations are uneven, and sentiment-driven pricing could unwind quickly if earnings fail to match lofty expectations.

Outside of Big Tech, the broader backdrop is more supportive than headlines suggest. U.S. economic data remains resilient, earnings season has exceeded expectations, inflation continues to trend lower, and monetary policy is easing as more rate cuts are expected and quantitative easing winds down. This creates opportunities away from the overvalued leaders, with many AI-related chip, cloud, and software companies still deserving evaluation on their own fundamentals rather than being treated as extensions of the Magnificent Seven. With signs of technical exhaustion emerging in the largest names, the era of effortless, tech-led gains may be maturing. Investors may need to wait for a healthier reset in Big Tech valuations while exploring new themes that offer growth without the same concentration risk.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategie

Basket of Income-generating ETPs

Ausschüttungsrendite

38.09%