Author

Jonathan Hobbs, CFA

Date

28 Nov 2024

Category

Market Insights

Options Gamma Explained: Straightforward Guide for Traders

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Options gamma is one of the lesser-known yet essential “Greeks” in options trading, especially for those keen on managing risk. While Delta measures how much an option’s price will change with a $1 move in the underlying asset, Gamma goes one step further. In this guide, we’ll unpack how Gamma works, why it matters, and how it interacts with Delta to shape your options strategy.

What is Gamma in options trading?

Gamma is the rate of change in an option’s Delta with a $1 change in the underlying asset’s price. In other words, Gamma measures how much Delta itself will rise or fall if the underlying asset’s price moves.

Think of it like this: while Delta measures an option’s “sensitivity” to price changes, Gamma measures “how fast” that sensitivity changes.

Here’s how it works for both call and put options:

Call options: Gamma is positive. As the stock price rises, Delta increases, making the call option more sensitive to further price changes.

Put options: Gamma is also positive. If the stock price drops, Delta becomes more negative, making the put option more sensitive to further downward price moves.

Why is Gamma important for options traders?

Gamma is especially useful for traders who are concerned with large and unexpected price moves. For example, stocks can move a lot with earnings announcements or major economic reports. Since Gamma measures how fast Delta changes, it’s crucial for traders who need to adjust their positions frequently.

Here’s why Gamma matters:

Delta stability: Higher Gamma means that Delta can shift quickly, causing an option’s price to respond more dramatically to price moves in the stock. This can be both a risk and an opportunity.

Risk management: Gamma helps traders understand how their portfolio’s sensitivity to price changes might evolve. This can be important for managing big, short-term positions.

Strategic adjustment: Traders with large options positions use Gamma to determine if and when they need to adjust their position, according to their risk tolerance.

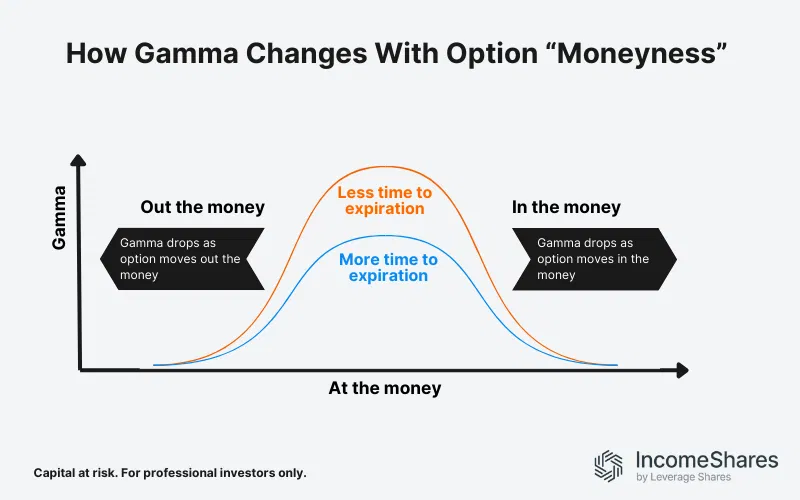

Gamma and Time Decay: Why gamma increases near expiration

Gamma changes based on how close the option is to expiration, and whether it’s in-the-money (ITM), at-the-money (ATM), or out-of-the-money (OTM).

At-the-money options: Gamma is highest for ATM options, especially as expiration approaches. That’s because there’s a high chance that small moves in the stock could push the option into profit (ITM) or loss (OTM).

Out-of-the-money and in-the-money options: Gamma is typically lower for OTM and ITM options. They’re less sensitive to small price moves since they’re already far from or close to the strike price.

Bottom Line: Gamma peaks as expiration nears, especially for ATM options. That means the option’s Delta will change faster with price movements in the underlying stock.

Example: How Gamma affects an option’s price

Let’s say you own a call option with a Delta of 0.5 and a Gamma of 0.1. If the stock price rises by $1, Delta will increase from 0.5 to 0.6 due to Gamma. This means the option is now more sensitive to further price changes, giving you higher potential profit if the stock keeps rising.

But if the stock moves against you, Gamma also means that Delta will change quickly – potentially increasing your loss if the option value falls.

Key takeaways

Gamma measures how much an option’s Delta changes with a $1 move in the underlying asset.

Higher Gamma means more Delta sensitivity, especially for ATM options near expiration.

Understanding Gamma can help you manage risk and adjust your options strategy for changing market conditions.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Cash-Secured Put + Equity

Distribution Yield

65.63%

Strategy

Cash-Secured Put + Equity

Distribution Yield

32.69%

Strategy

Cash-Secured Put + Equity

Distribution Yield

42.62%

Strategy

Cash-Secured Put + Equity

Distribution Yield

52.91%

Strategy

Covered Call

Distribution Yield

12.10%