Author

Violeta Todorova

Date

10 Feb 2026

Category

Market Insights

Magnificent Seven: AI Growth Faces Harsh Capex Check

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

The Magnificent Seven: Market Leaders Facing a New Reality

For much of the past decade, U.S. equity performance has been defined by a single group of stocks. The Magnificent Seven: Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta and Tesla did not simply outperform the market; they became the market.

Their dominance was built on a powerful combination of asset-light business models, expanding margins, relentless earnings growth and balance sheets strong enough to fund buybacks, dividends and strategic investment simultaneously. That model worked exceptionally well but today, this backdrop is changing and with it, the rules of leadership.

From Asset-Light Giants to Capital-Heavy Operators

The current change now unfolding is structural rather than cyclical. The Magnificent Seven are transitioning from cash-generative, asset-light platforms into capital-intensive infrastructure builders, driven primarily by artificial intelligence.

AI is no longer a software story alone. It is a datacentre, power, networking and semiconductor story and that comes with an enormous price tag. Across the largest hyperscalers, capital expenditure is accelerating sharply, consuming a growing share of operating cash flow.

This matters because the very characteristics that once justified premium valuations such as high margins, low reinvestment needs and abundant free cash flow are now being diluted. Buybacks are becoming less generous, balance sheets are expanding, and returns are being pushed further into the future.

The market is not questioning the importance of AI. It is questioning how long investors are willing to wait to be paid.

Leadership Is Expanding Beyond Big Tech

While headline indices still appear resilient, leadership is clearly broadening. Performance is no longer being driven exclusively by mega-cap technology. Despite the stress in parts of technology, the broader market has not unravelled in the same way. Dispersion across stocks has increased, which has helped keep headline volatility contained even as individual sectors experience large moves. The equal-weight S&P 500 benchmark has pushed to a record and continues to outperform its market-cap-weighted counterpart. This shows how much performance has broadened away from the largest growth names. Several industry groups, including energy, materials, food and beverage, transportation, pharmaceuticals and even tech hardware and equipment, are sitting at or near highs, reinforcing the sense that the market is rotating.

This rotation reflects a change in investor priorities. As inflation pressures ease, capital is increasingly flowing toward businesses tied to real economic activity, domestic investment and tangible cash generation. When volatility is being absorbed through dispersion rather than broad sell-offs, this is a sign of a maturing bull market rather than the end of one.

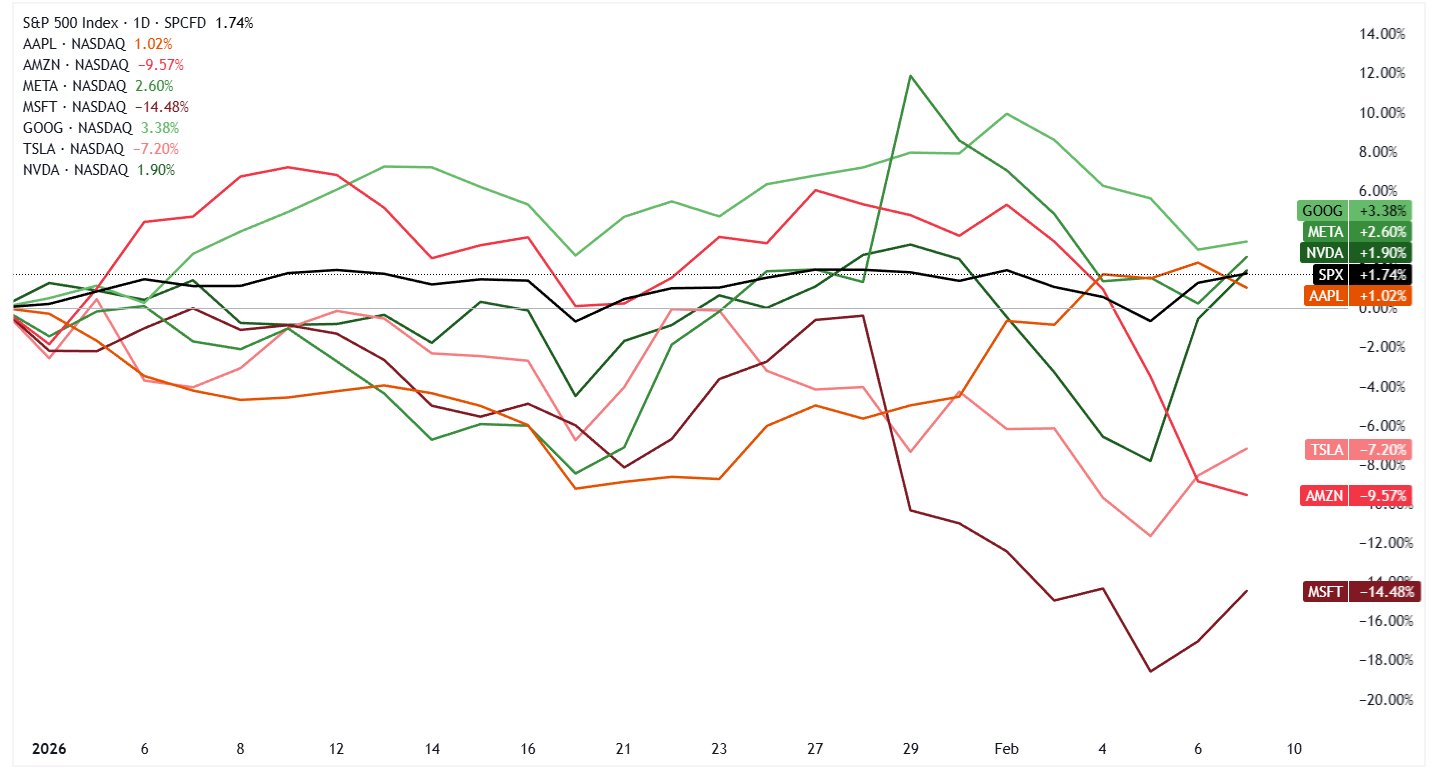

Source: TradingView. Magnificent 7 vs S&P 500, YTD daily price chart as of 10 February 2026.

AI: From “At Any Price” to “Show Me the Returns”

The AI trade itself is changing. Early enthusiasm rewarded anything associated with artificial intelligence, regardless of cost or capital intensity. That phase is ending and the market is now separating AI enablers from AI spenders, monetisers from infrastructure builders, and cash-flow generators from balance-sheet expanders.

This is evident in the growing dispersion within the Magnificent Seven. Some stocks are being rewarded for discipline and execution, while others are being penalised despite strong top-line growth.

The key question is no longer whether AI demand exists. It is whether that demand can be translated into sustainable margins and free cash flow in the near-term.

Capital Expenditure Becomes the Central Risk

The current earnings season highlighted how sensitive markets have become to capital allocation.

Several mega-cap technology companies delivered strong operational results: solid revenue growth, expanding user bases and robust demand for AI-related services. Yet share prices fell as investors reacted to the scale and persistence of capital expenditure commitments.

When annual investment plans begin to approach, or even exceed, operating cash flow, valuation frameworks inevitably change. Earnings growth remains important, but capital efficiency now carries far more weight.

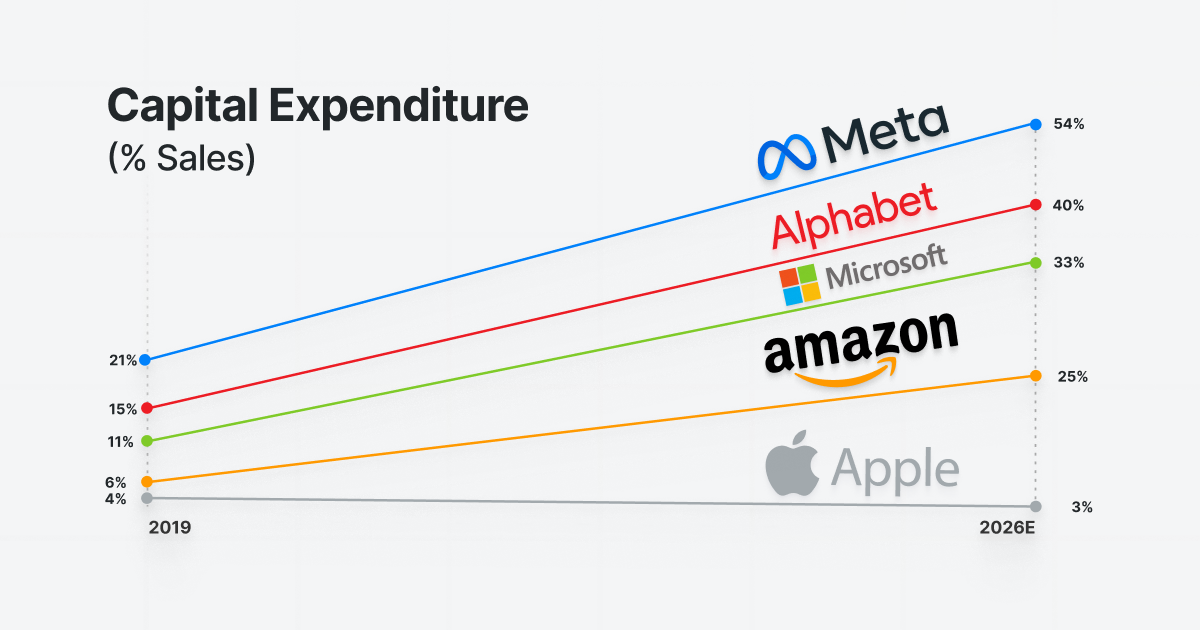

Source: Leverage Shares. Magnificent Seven estimated capex as percentage of sales.

Magnificent Seven Earnings: Still the Engine of Growth

Despite these concerns, the Magnificent Seven still remain the primary earnings engine of the U.S. market.

Combined earnings growth continues to significantly outpace the rest of the index, supported by strong revenue expansion, global scale and dominant competitive positions. Looking ahead, the group is expected to contribute more than a quarter of total S&P 500 earnings, underscoring their continued importance.

However, the market is clearly applying a higher bar. Premium valuations are no longer granted automatically, they must be justified through execution, discipline and credible monetisation pathways.

Inside the Magnificent Seven: Diverging Paths Emerge

Apple: Discipline is a Competitive Advantage

Apple stands out for its restraint. Strong iPhone demand, an expanding installed base and stable services growth continue to support robust cash generation. Its approach to AI is focused on integration, partnerships and targeted investment rather than massive infrastructure build-outs and as such preserves flexibility and protects margins.

Meta: Cash Flow Funds Ambition

Meta’s advertising engine is generating the cash flow needed to fund aggressive AI investment without destabilising the balance sheet. While margins may fluctuate, the company retains the ability to self-finance its ambitions, which the market continues to reward.

Amazon and Alphabet: Scale Comes at a Cost

Both companies are executing well operationally, particularly in cloud and AI-related services. The challenge lies in the magnitude of ongoing investment. Markets are increasingly cautious about open-ended capex cycles, despite being backed by high-quality businesses.

Microsoft: Strategic Positioning but Near-Term Trade-Offs

Microsoft remains central to enterprise AI adoption, but accelerating investment is weighing on margins. The long-term opportunity is clear but the near-term trade-off between scale and profitability is now front and centre.

Tesla: Optionality Under Scrutiny

Tesla continues to invest heavily in AI, autonomy and robotics, but near-term fundamentals are under pressure. The market is becoming less willing to price long-dated optionality without clearer visibility on cash flows.

Nvidia: The Final and Most Important Test

Nvidia remains the final Magnificent Seven member yet to report, and expectations are exceptionally high. Earnings and revenue growth are projected to remain explosive, reinforcing Nvidia’s role as the primary enabler of the AI infrastructure boom.

More than any other result this season, Nvidia’s report would impact sentiment toward the entire group. Continued outperformance would strengthen confidence that today’s capex surge is justified. Any sign of slowing momentum would intensify scrutiny on AI spending across the sector.

Conclusion:

The Magnificent Seven remain exceptional businesses with unrivalled scale, global reach and strategic importance. They continue to drive earnings growth and lead long-term innovation.

But investors are no longer paying simply for growth or ambition. They are paying for capital discipline, cash-flow durability and proven monetisation. Leadership is fragmenting, valuations are being tested, and execution matters more than ever.

Professional investors looking to invest in the Magnificent Seven may consider IncomeShares Magnificent 7 Options ETP.

The Magnificent 7 Options ETP offers exposure to the performance of the underlying basket and seeks to generate monthly income. Each component is weighted equally and rebalanced semi-annually.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Basket of Income-generating ETPs

Distribution Yield

55.84%