Author

Jonathan Hobbs, CFA

Date

18 Feb 2025

Category

Market Insights

Assignment Risk Explained: What It Means for Options ETPs

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Some options-based ETPs are designed to generate income, but they come with unique risks. One of the most important (and often overlooked) is assignment risk. Assignment happens when an options seller is required to fulfill the contract, meaning they must buy or sell the underlying asset at the strike price before expiration.

For options ETPs that sell calls or puts, this can impact performance, risk management, and cash flow. Here’s how assignment risk works, why it happens, and what it means for investors in covered call and put-write strategies.

What is assignment risk?

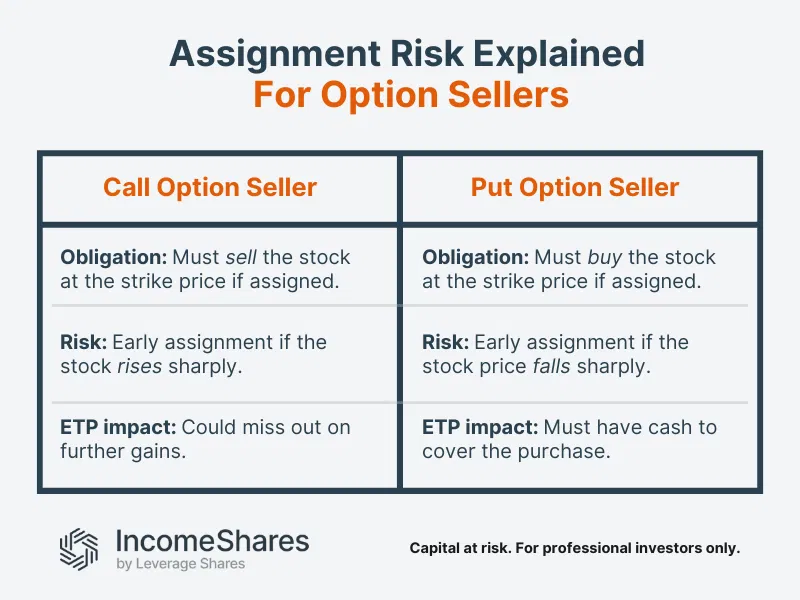

If you sell an option, you take on the obligation to fulfill the contract if the buyer chooses to exercise.

Call sellers must sell the stock at the strike price.

Put sellers must buy the stock at the strike price.

For most options traders, assignment is rare because many options are closed out before expiration. But for options-based ETPs, assignment is a constant risk – especially with American-style options, which can be exercised any time before expiration.

How assignment risk works in options ETPs

Unlike European options, which can only be exercised at expiration, American-style options allow early exercise. This means ETPs selling call or put options can be assigned unexpectedly.

Example: Covered call early assignment

A covered call ETP sells call options on a stock that pays dividends.

If the stock price rises before the ex-dividend date, call holders may exercise early to capture the dividend.

The ETP must then sell the stock at the strike price – missing out on further gains.

In-the-money (ITM) options typically have higher assignment risk

The deeper an option moves in the money, the higher the chance of assignment.

If a call option’s strike price is far below the current stock price, it’s more likely to be exercised early.

If a put option’s strike price is far above the stock price, early assignment risk increases.

This matters for put-writing ETPs, which sell put options to generate income. If the market drops sharply, put holders may exercise early – forcing the ETP to buy the stock at the strike price before expiration.

0DTE put-writing and assignment

0DTE (zero-days-to-expiration) put-write ETPs sell put options that expire the same day. This generally reduces assignment risk because:

Most 0DTE options expire worthless, as they are short-term bets on market movements.

Traders rarely exercise 0DTE options early because they typically close their positions instead.

ETPs selling 0DTE puts avoid overnight exposure, lowering the chance of unexpected assignments.

Since 0DTE options have limited time to move deep in the money, early assignment is less of a concern compared to longer-dated options strategies.

Managing assignment risk in options ETPs

For investors in covered call and put-write ETPs, assignment risk affects strategy execution.

Limits upside potential: If a call option is assigned early, the ETP must sell the stock at the strike price, capping gains.

Stock turnover: Assigned shares may need to be replaced, affecting portfolio rebalancing.

Cash reserves: Put-write ETPs typically hold sufficient cash to cover potential early assignments. This helps ensure the fund can meet its obligations without needing to sell other assets.

Cash-secured put strategies: Many put-write ETPs use a cash-secured approach. That means they set aside enough capital to buy the underlying asset at the strike price if assigned. This helps manage risk and maintain liquidity.

At IncomeShares, our options-based ETPs actively seek to manage assignment risk.

Key takeaways

Assignment happens when an options seller is required to fulfill the contract early.

Options-based ETPs can face early assignment, especially with deep ITM options.

0DTE put-writing strategies generally have lower assignment risk than longer-dated put-writing strategies.

Active management can help reduce early assignment risk and optimize returns.

Your capital is at risk if you invest. You could lose all your investment. Please see the full risk warning here.

Related Products:

Strategy

Cash-Secured Put + Equity

Distribution Yield

54.86%

Strategy

Cash-Secured Put + Equity

Distribution Yield

64.85%

Strategy

Cash-Secured Put + Equity

Distribution Yield

49.37%

Strategy

Cash-Secured Put + Equity

Distribution Yield

100.62%

Strategy

Covered Call

Distribution Yield

11.61%